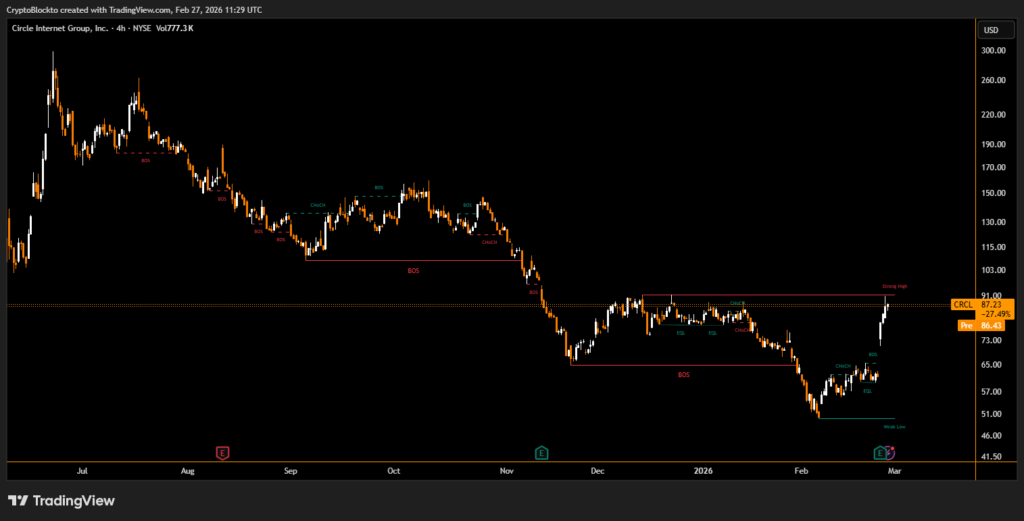

Shares of Circle briefly topped $90 following a strong Q4 report, extending post earnings gains driven by expanding revenue streams beyond traditional reserve income. Analysts at Bernstein reiterated an outperform rating with a $190 price target, citing “clear divergence from crypto” as Circle’s revenue and adjusted EBITDA exceeded expectations.

Transaction revenue strengthened, supported by Circle’s super validator role on the Canton blockchain network and an increase in USDC held directly on Circle’s platform to 17% of total supply, up from 14% the prior quarter. Circle projects USDC circulation to grow 40% annually, with other revenue sources potentially reaching $170 million in 2026.

Prediction Markets and Agentic Commerce Drive Adoption

Mizuho analysts raised their Circle price target to $90, highlighting activity on prediction markets such as Polymarket as a key driver of USDC usage and high-velocity transaction flows. The firm also noted potential long-term demand from “agentic AI” applications, where autonomous software agents may require internet-native money, though current adoption remains small.

While revenue diversification supports optimism, Mizuho cautioned that interest-rate changes could weigh on reserve income, which still forms the majority of Circle’s earnings. Analysts continue to monitor how the stablecoin issuer balances growth from emerging payment and DeFi use cases with traditional reserve-based income.

Disclaimer

This content is for informational purposes only and does not constitute financial, investment, or legal advice. Cryptocurrency trading involves risk and may result in financial loss.