Ongoing uncertainty around stablecoin regulation could place traditional financial institutions at a disadvantage compared with crypto-native firms. According to Colin Butler, banks have already invested heavily in digital asset infrastructure but remain hesitant to deploy it fully while policymakers debate how stablecoins should be classified.

Legal teams at many financial institutions are reportedly advising caution until regulators clarify whether stablecoins will be treated as deposits, securities or a new form of payment instrument. Several large banks have already developed key infrastructure components, including blockchain payment networks, digital asset custody services and tokenized deposit experiments.

Yield Differences Could Pressure Traditional Bank Deposits

The growing gap between returns offered by stablecoin platforms and traditional savings accounts is also drawing attention. Butler noted that some crypto exchanges provide yields between 4% and 5% on stablecoin balances, while typical savings accounts offer less than 0.5%.

Analysts say such differences could gradually encourage deposit migration if digital dollar products become widely accepted as everyday financial tools rather than trading instruments.

Restrictions on Stablecoin Yield Could Push Activity Offshore

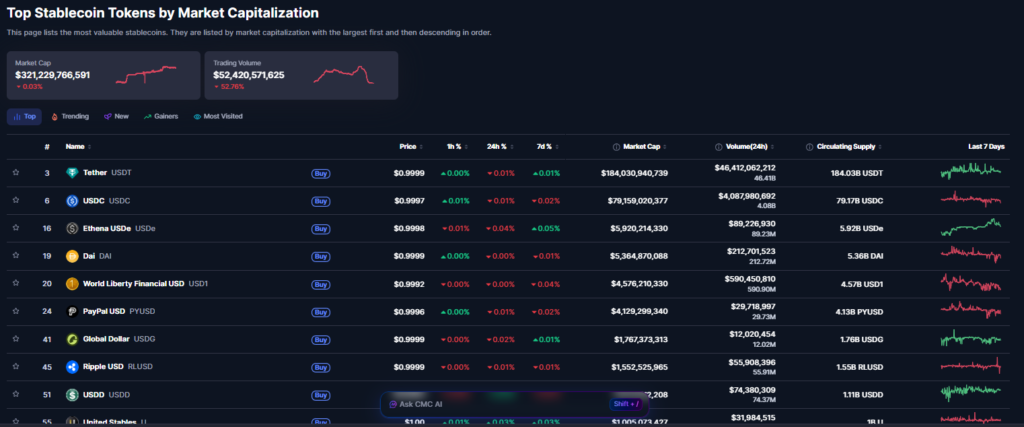

Some experts warn that strict limits on stablecoin yields could produce unintended consequences. Alternative products such as USDe demonstrate how digital assets can generate returns through derivatives markets rather than traditional reserves.

If regulations tighten too aggressively, capital may shift toward offshore or synthetic structures where oversight is weaker, potentially increasing systemic risk rather than reducing it.

Disclaimer

This content is for informational purposes only and does not constitute financial, investment, or legal advice. Cryptocurrency trading involves risk and may result in financial loss.