The Financial Action Task Force (FATF) has raised fresh concerns that stablecoins are increasingly being used to circumvent sanctions and anti-money laundering controls, particularly through peer-to-peer transfers conducted via self-custody wallets.

FATF Report on Stablecoins and AML Gaps

In its latest targeted review, the FATF highlighted structural vulnerabilities within the stablecoin ecosystem. Transactions executed directly between users through unhosted, or self-custody, wallets can take place without the involvement of regulated intermediaries such as exchanges or custodians.

This absence of oversight creates potential blind spots in Anti-Money Laundering (AML) and counterterrorism financing frameworks. While blockchain transactions remain permanently recorded on public ledgers, the pseudonymous nature of wallet addresses makes identifying the individuals behind transfers more complex.

Peer-to-Peer Stablecoin Transfers Under Scrutiny

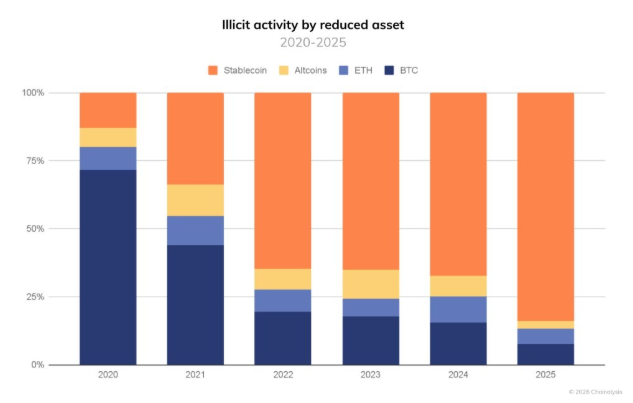

According to blockchain analytics firm Chainalysis, illicit cryptocurrency addresses received at least $154 billion in 2025, with stablecoins accounting for 84% of that activity. However, illicit transactions still represented less than 1% of total crypto transaction volume, underscoring that the majority of usage remains legitimate.

The FATF is urging jurisdictions to assess the risks linked to stablecoin arrangements and apply proportionate safeguards. Suggested measures include enhanced monitoring when self-custody wallets interact with regulated platforms and clearer compliance obligations for stablecoin issuers and distributors.

As stablecoins expand into payments and cross-border settlements, regulators are increasingly focused on closing compliance gaps without stifling financial innovation.

Disclaimer

This content is for informational purposes only and does not constitute financial, investment, or legal advice. Cryptocurrency trading involves risk and may result in financial loss.