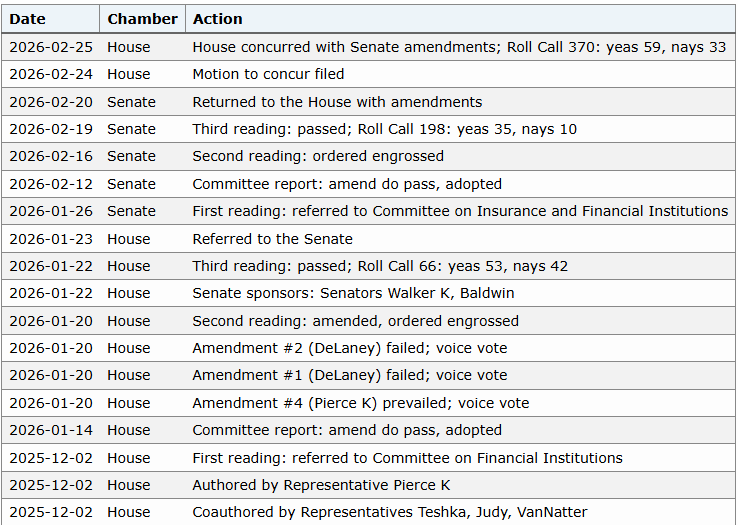

Indiana lawmakers have passed House Bill 1042 (HB1042), a landmark piece of legislation aimed at protecting cryptocurrency users and promoting digital asset investment options. The bill cleared both chambers with 59 votes in favor and 33 against and now awaits signature from Governor Mike Braun. If signed, the legislation would take effect on July 1, 2026, with certain provisions, including crypto options in retirement plans, activating later.

HB1042 prohibits discriminatory taxes on cryptocurrencies and restricts state and local agencies from enacting rules that block lawful crypto payments, self-custody, or mining operations. It also extends protections to public employees, teachers, and other state workers by allowing participation in retirement plans that include self-directed brokerage accounts with at least one cryptocurrency investment.

Retirement Plans to Include Crypto Options

The bill is notable for requiring certain state retirement and savings plans to provide crypto investment options, potentially starting July 1, 2027. This includes Indiana’s defined contribution plans, the Hoosier START plan, and specified teachers’ and public employees’ retirement funds, allowing citizens to hold Bitcoin and other digital assets as part of their long-term savings strategy.

Indiana joins a growing list of states enacting crypto-friendly legislation, distinguishing itself by formally integrating crypto into retirement plan options while safeguarding investor rights against restrictive state regulations.

Disclaimer

This content is for informational purposes only and does not constitute financial, investment, or legal advice. Cryptocurrency trading involves risk and may result in financial loss.